EU Corporate sustainability reporting directive (CSRD)

The Corporate sustainability reporting directive (CSRD) is a new EU mandate for large and public companies starting in 2025, extending to smaller companies by 2026. It modernizes social and environmental reporting, making sustainability reporting as crucial as financial reporting. Companies must disclose their sustainability performance across environmental, social, and governance (ESG) aspects.

Sustainability performance and reporting are well known in the maritime industry and there has been a gradual development of the requirements for more than two decades. The most common reporting standards for maritime companies have been the Global Reporting Initiative (GRI, 1997) and the Sustainability Accounting Standards Board (SASB, 2011).

The European Sustainability Reporting Standards (ESRS) are the standards that underpin the CSRD. The ESRS standards contain more than 1000 data points and more than 800 of them are mandatory depending on the result of your double materiality assessment. ESRS is significantly more comprehensive than SASB covering the entire value chain of the reporting company.

Some of the key new requirements with CSRD are:

- Limited Assurance. ESG performance and report to be audited by accredited

company - Double Materiality Assessment. The Double Materiality Assessment involves

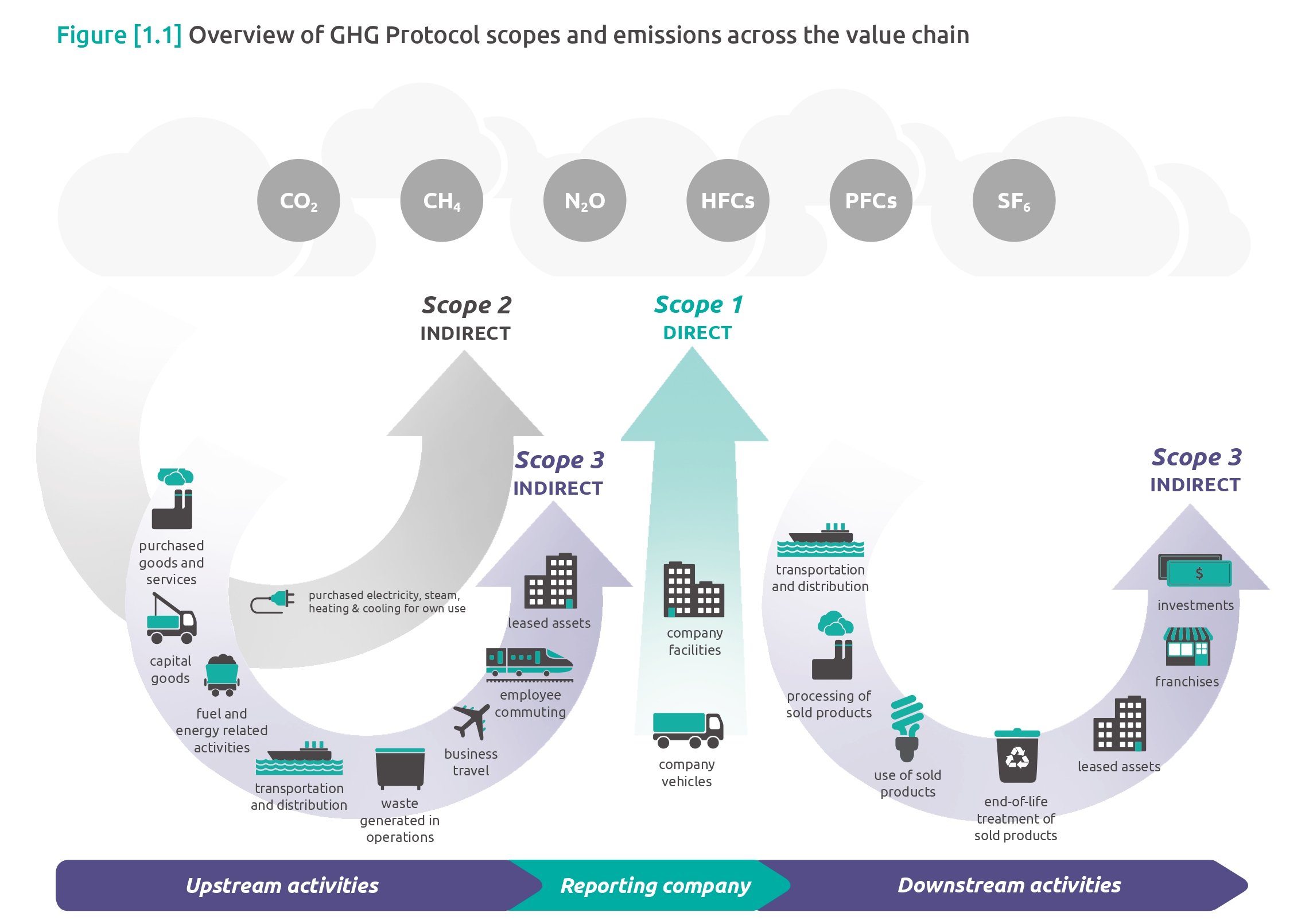

evaluating sustainability matters from two perspectives: Financial Materiality (outside-in perspective) focuses on how sustainability matters may pose risks or opportunities that could affect a company's financial performance and position over the short, medium, and long term. Impact Materiality (inside-out perspective) focuses on the impacts on people or the environment that are directly linked to a company's and its value chain operations. - Scope 1, 2 and 3 reporting. Scope 1 emissions are direct greenhouse gas (GHG) emissions that occur from sources that are controlled by an organization, e.g. ships on CoA, Voyage Charter, T/C-in. Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling, e.g. office buildings and shore power. Scope 3 emissions are all other indirect emissions that occur in a company’s value chain, E.g. T/C out, ship building, maintenance, spare parts, Well-to-tank emissions etc.

- Transition plans. This plan outlines the company's strategy to address climate impact and prepare for climate risks. It includes setting out clear targets, actions, and timelines for reducing emissions and transitioning to a sustainable business model.

DNV has long experience in assisting maritime clients related to improving and documenting sustainability performance and we recommend our clients to start early, preferably more than a year ahead, preparing for CSRD. It takes time to incorporate changes to the ESG-reporting and it is much better to finish early than rushing to the end.

This article was made exclusively for the subscribers of our quarterly newsletter. To subscribe, and receive tailored news and regulatory updates on shipping in Norway, sign up here: DNV Maritime om Norsk Skipsfart

12/13/2024 3:31:00 PM