Costly capital: Money for green megawatts in Sub-Saharan Africa

Small gains in lowering the cost of capital have big effects in Sub-Saharan Africa’s ability to finance critically needed green electricity. With countries updating climate plans ahead of COP30, now is the time for smart thinking about finance flows for energy buildout in the region.

By Anne Louise Koefoed and Sujee Selvakkumaran

Climate compatible development paths depend on costs and access to finance

In 2025 – the midpoint of a critical climate action decade – parties to the Paris Agreement are expected to submit their second Nationally Determined Contributions (NDCs) with a timeframe for implementation through to 2035. NDCs are key to enhancing ambitions and accelerating emission reduction achievements as originally intended in the Paris Agreement set-up. NDCs chart the energy plans of countries and therefore point to the planned direction for opportunity and energy investments.

At time of writing, only a few countries have submitted their new plans within the deadline of 10 February 2025. In fact, 95% of countries have missed the deadline (Carbon Brief, 2025). But the period for NDC submissions until September, when a synthesis report will be prepared for the next Climate Change Conference (COP), is a critical period for smart thinking about the international dimension of climate-policy approaches including access to capital to catalyse new renewable power investments and raise their attractiveness to private investors.

Sub-Saharan Africa: the missing money problem

The energy development path of emerging regions, especially Sub-Saharan Africa (SSA), is crucial for a decarbonized future. Currently, half the region’s population lacks electricity (UNCTAD, 2023), and demand is set to nearly double from 22.2 EJ in 2024 to 40 EJ by 2050 (DNV, 2024) as populations and economies grow. Expanding power generation using SSA’s vast renewable resources is essential, but financing remains the key bottleneck.

SSA faces a severe funding gap, falling far short of the USD 20 billion in annual investment needed to meet SDG-7 by 2030 (IEA, 2020), with estimates suggesting only USD 8 billion is being funded annually (Hafner et al., 2018). Given competing demands on limited public funds, bridging this gap requires external capital without increasing debt burdens.

A mix of private, public, and international finance is essential to scale investments in clean power. Development finance institutions, such as the African Development Bank, will be critical in mobilizing concessional loans, grants, and co-investment while helping investors manage risks in SSA’s emerging renewable energy markets.

Without funding and risk mitigation measures, emerging, low-income economies will be prevented from leveraging the benefits and cost savings offered by the plummeting costs of renewable energy technologies.

Transition policy ambitions are contingent on international support

Our review of country pledges (‘existing’ NDCs) in Sub-Saharan Africa suggests a regional target of not growing emissions more than 68% by 2030 relative to 1990. However, these targets are conditional on international support.

Renewable power is the ‘first mover’ sector in the energy transition: it is critical for increasing electricity access and preventing conventional fossil-fuel based development. 28 countries in the Sub-Saharan Africa region signed the COP28 Global Renewables and Energy Efficiency Pledge, and several countries in the region have set renewable generation targets. These targets vary widely. For example, the ECOWAS countries aim for a 19% share of generation from new renewables in the electricity mix by 2030, Nigeria is aiming at 36%, South Africa 41%, and Kenya is going for 100% in 2030 from renewable power generation. South Africa’s Renewable Energy Masterplan (SAREM 2023) also sets capacity targets, adding 22.9 GW of utility-scale renewable energy and battery storage by 2030.

Where investment requirements to meet the energy transition agenda are reported (e.g. by Ghana in September 2023, and Nigeria in August 2022), they do not reflect existing domestic policy and funding but underline financing needs. For example, about USD 410bn above business-as-usual spending is needed in Nigeria between 2021 and 2060 (SEforALL, 2022). Clearly, a significant boost of investment flows into the Sub-Saharan African region is needed if is to make progress towards its renewable energy targets.

A financing trickle

Sub-Saharan Africa urgently needs new electricity generation to improve energy access and support industrial growth. However, the region has lagged in global energy investment, receiving just 3% of total energy funds and 1.5% of renewables between 2010 and 2020—dropping to less than 1% since (IRENA et al., 2023). Moreover, financing is unevenly distributed, with a few countries receiving the bulk, while the 33 least-developed nations secured only 37% of renewable commitments from 2010 to 2019 (IRENA, 2024).

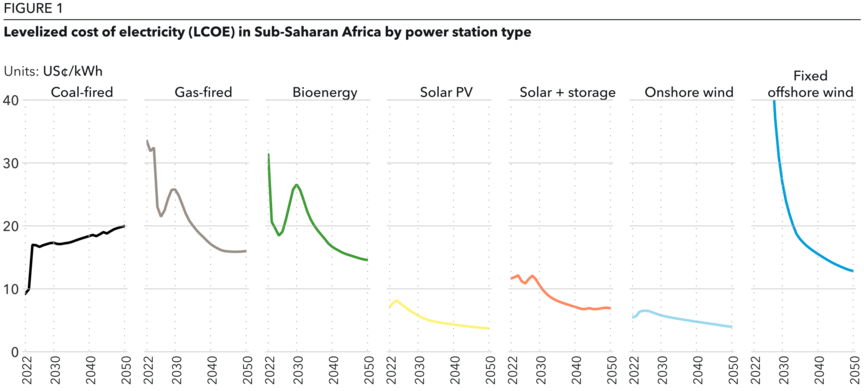

This decline in investment contrasts with growing opportunities for non-fossil energy. As shown in Figure 1, the levelized cost of electricity (LCOE) for renewables is at an all-time low, making solar PV, onshore wind, and storage more viable than ever.

Despite the manifold benefits of green electrotechnology, our analysis shows that, until 2023, most capital expenditure (CAPEX) in the power sector was directed toward fossil-fuel power plants. On average, between 2015 and 2024, for every 3 USD invested in fossil-fuel power plants, only 1 USD was invested in solar and wind in the region. However, in 2023, for the first time in Sub-Saharan Africa’s history, investments in solar and wind power surpassed those in fossil-fuel power.

The main reason for the previous lack of investment in solar and wind lies in the structure of capital financing. Large, centrally planned fossil-fuel projects typically benefit from state-guaranteed funding. To attract more investment into renewable power, it is crucial to enable the free flow of capital — which requires providing risk-guaranteed funding.

The success of utility-scale renewables hinges on an enabling policy environment, technical support, and international capital—particularly concessional finance and development bank funding to catalyze private investment. This highlights the critical role of COP29’s finance agenda and the New Collective Quantified Goal (NCQG) in de-risking private capital flows.

New Collective Quantified Goal agreed at COP29

At COP29 in Baku, negotiators agreed to triple climate finance from developed to developing countries, setting a new target of USD 300 billion annually by 2035. This New Collective Quantified Goal (NCQG) replaces the COP15 commitment of USD 100 billion per year by 2020, which was only met in 2022 with USD 116 billion (OECD, 2024).

NCQG funding aims to boost clean energy investment and climate resilience, contributing to a broader goal of mobilizing USD 1.3 trillion annually from public and private sources by 2035 (UNCTAD, 2024). It is also key to scaling up Nationally Determined Contributions (NDCs), ensuring climate targets remain viable amid geopolitical uncertainties.

Cost of Capital - the decisive factor in getting renewable projects off the ground

The financing structure of renewable energy investments varies widely across Sub-Saharan Africa, with projects ranging from fully debt-financed to fully equity-financed models.

For instance, in South Africa, our sources there confirm that most renewable energy projects are predominantly financed through debt capital, whereas in Senegal, concessional finance ─ debt offered at lower interest rates ─ and equity play a more significant role (IEA, 2025).

Both debt and equity capital carry associated costs. The cost of debt is reflected in interest payments, while the cost of equity represents the opportunity cost of invested capital. This overall cost of capital (CoC) is a key determinant of whether a renewable energy project, such as a solar PV power plant, proceeds to implementation.

The cost of capital is influenced by the level of risk associated with the project. Two primary risk factors impact financing: technology risk and geographic risk. If a technology and its supply chain are not well established, the perceived project risk is higher, leading to an increased CoC. Even for mature technologies like solar PV, projects located in high-risk regions, such as many parts of SSA, face a ‘risk premium’ which raises the CoC compared with lower-risk regions.

A complex set of economic, political and institutional factors commonly emphasized in authoritative resources (e.g. IMF, 2024; IEA, 2023) contributes to increase the risk premium demanded by investors, including:

- Political & Security Risks: War, civil unrest, expropriation, and property rights concerns.

- Sovereign Credit Risks: Debt burdens, declining credit ratings, and high capital costs for imported renewable technology.

- Currency Risks: Exchange rate volatility and depreciation, affecting revenue stability for projects earning in local currency.

- Energy System Risks: Weak utilities, infrastructure deficiencies, off-taker solvency issues, and stalled electricity sector reforms hindering independent power producers.

In our Energy Transition Outlook (ETO) analysis and modelling, we reflect such risks when incorporating assumptions about the CoC across different power technologies and our ten global regions (DNV, 2024). Europe, with well-established renewable energy infrastructure, is considered one of the least risky regions for investment in solar PV and wind, whereas the Sub-Saharan Africa region faces significantly higher financing challenges due to elevated risk .

The cost of costly capital illustrated by solar deployment

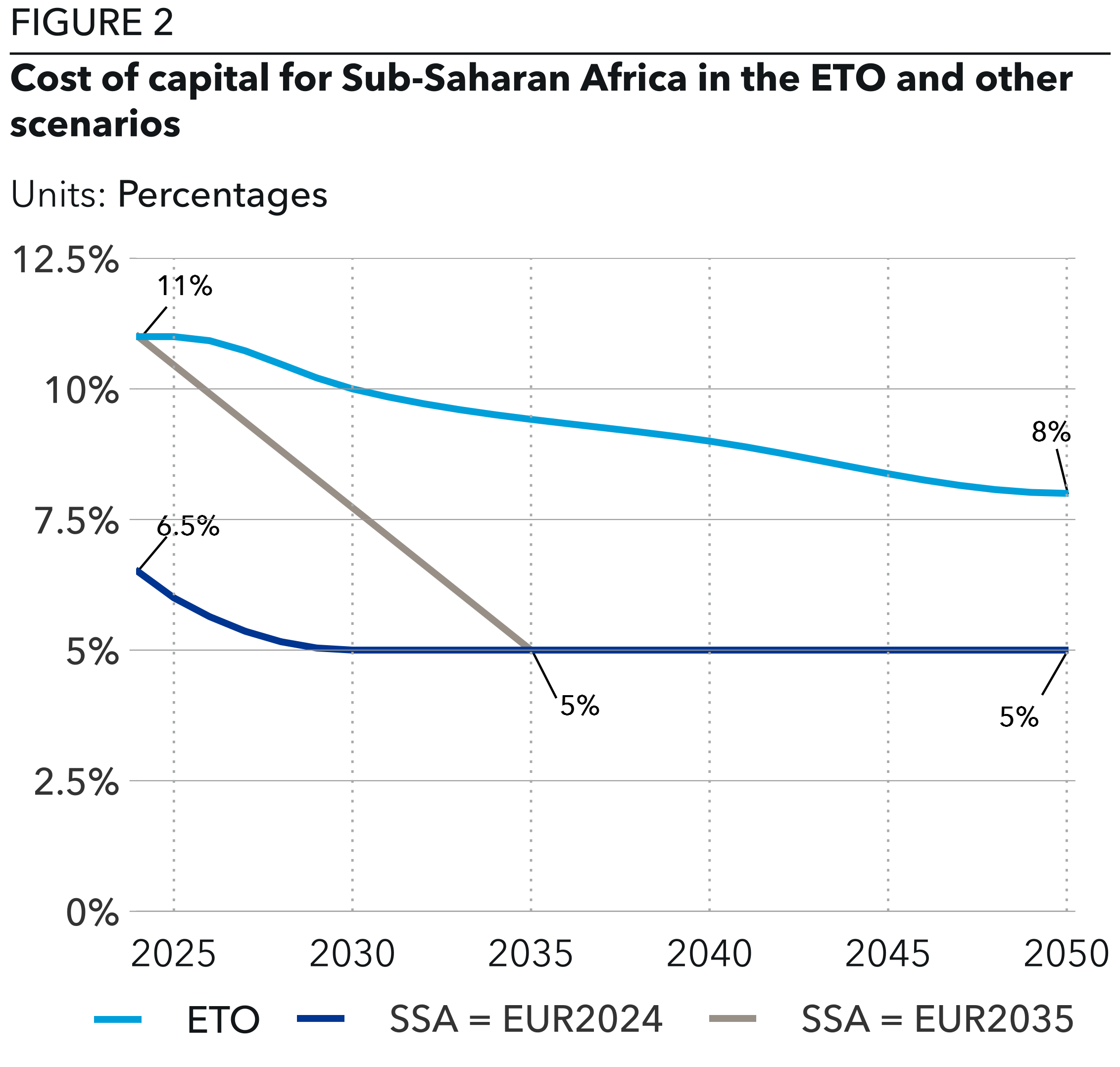

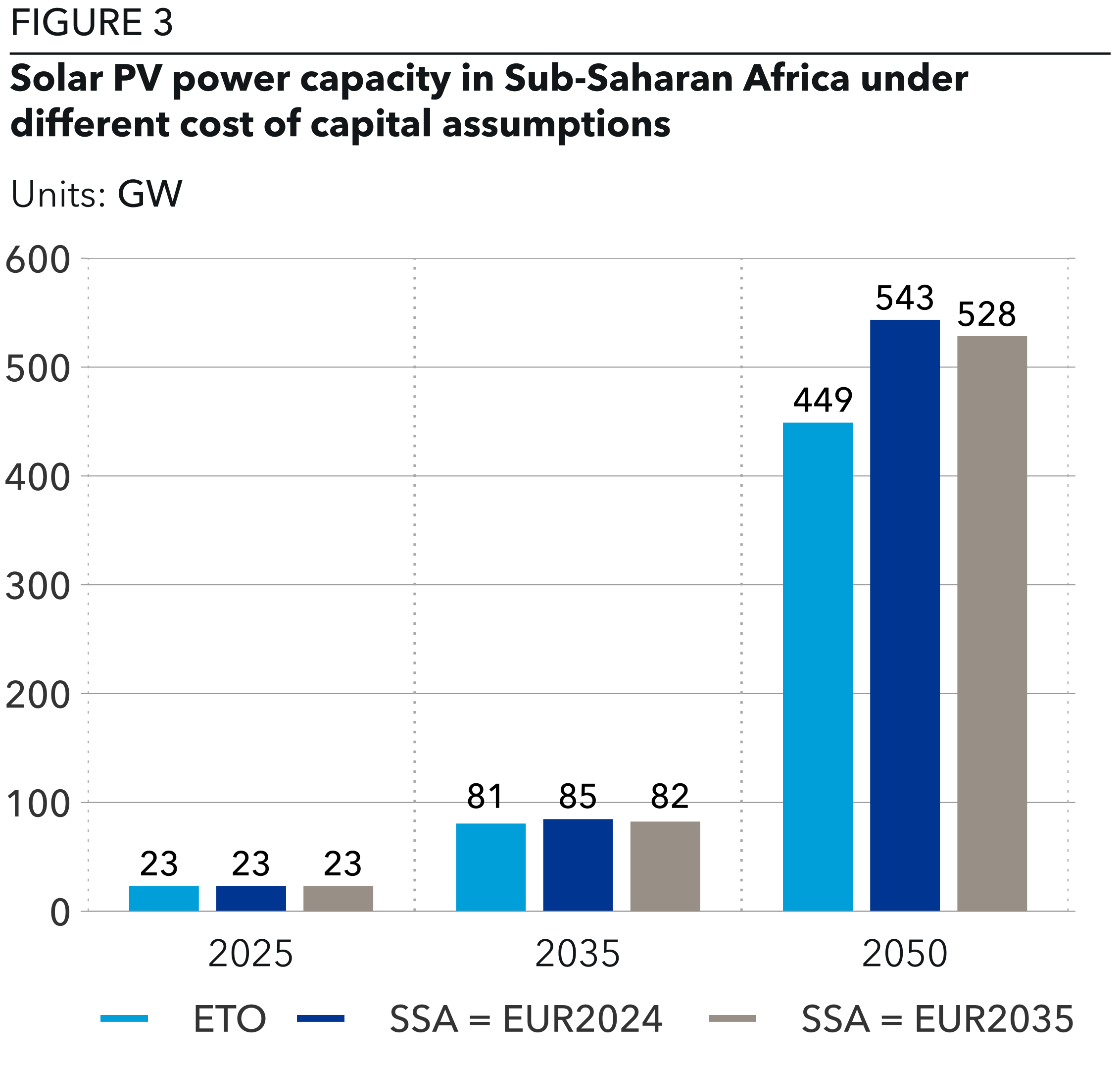

We modeled two scenarios to assess how varying cost of capital (CoC) assumptions affect future solar PV capacity in Sub-Saharan Africa (SSA) compared with our ETO baseline.

Figure 2 illustrates different CoC trajectories. The light blue line represents the baseline ETO assumption for SSA, while the dark blue line (European CoC) highlights the region’s risk premium. We also explore two alternatives: one where SSA adopts Europe’s CoC from 2024 to 2050 and another (grey line) where SSA’s CoC gradually converges to Europe’s within a decade.

By 2050, under the ETO baseline forecast, SSA is projected to have approximately of installed solar PV capacity, with the cost of capital (CoC) assumed to decline from 11% in 2024 to 8% by mid-century (Figure 2 light blue).

However, if SSA had a CoC equivalent to that of Europe throughout the period from 2024 to 2050, the region’s solar PV capacity could reach almost 545 GW by 2050 ─ nearly 100 GW more

While 80 GW of solar capacity may seem modest, it’s important to consider the current electricity consumption levels in the region. A typical household in Sub-Saharan Africa consumes approximately 1,000 kWh per year at best (Tamele et al., 2025). Based on this, 80 GW of solar power could supply electricity to around 4.3 million households at current consumption rates. Although electricity consumption ─ and with it, the standard of living ─ is expected to rise over time, any additional renewable power capacity remains invaluable in addressing the region’s energy needs.

The time to act is now

In the near term, up to 2035, the impact of the reduction in the CoC for solar PV is expected to remain limited. There are two primary reasons for this. First, most of the power plants set to come online in the coming years have already been planned, with financial investment decisions made to meet projected capacity needs.

Second, the marginal benefits of lower CoC ─ driven by decreasing solar PV costs ─ take time to accumulate and compound through cost-learning effects. This time lag is a key component of the systemic inertia often seen in large socio-technical systems (Singh et al., 2019). Achieving a critical reduction in both solar PV costs and financing costs in Sub-Saharan Africa requires time for this reinforcing cycle of cost reduction to take effect.

Beyond the initial five to ten years, however, the compounding benefits of cost reductions and technological learning gain enough momentum to overcome this inertia. This is evident in the differences in solar PV adoption between the ETO baseline forecast and scenarios where Sub-Saharan Africa’s CoC either matches or converges toward Europe’s. Ultimately, the CoC for renewables in this decade is crucial in shaping long-term outcomes. Therefore, the time to act and de-risk the Sub-Saharan African region for renewable investment is now.

Risk mitigation instruments to lower the cost of capital

We have shown the difference in buildout resulting from lowering the cost of capital. Our findings illustrate the need for de-risking measures that contribute to renewable energy project viability (financial close and operational phase), attract investments and level the playing field in terms of risk premia.

There are multiple concrete ways to lower the CoC of renewable power projects in SSA.

- Legally binding PPAs: Power purchase agreements (PPAs) with off-takers, such as state-owned utilities, independent power providers, or large energy consumers like data centres and mining companies, enhance investment security. In South Africa and Botswana, solar projects commonly use PPAs with local utilities (Personal communication, 2025).

- Sovereign guarantees: Government-backed guarantees mitigate default risks, making projects bankable and unlocking lower-cost financing.

- Development finance & risk insurance: Institutions like MIGA (World Bank) and the Norwegian NORAD’s Guarantee Scheme can insure against currency fluctuations, sovereign defaults, and political risks, using their financial capacity to de-risk renewable energy investments.

Relevant risk mitigation options exist and are comprehensively described elsewhere (Calcaterra et al., 2024; IRENA, 2016; Duma et al., 2024). Solidifying such instruments with long term coverage and a resolve on climate finance commitments would help overcome hindrances to both clean power investments and ambitious mitigation strategies for the 2025 NDC updates.

Why is investing in Sub-Saharan Africa key for global growth?

Recent funding cuts to key multilateral agencies, including USAID, threaten global cooperation on renewable energy and electrification in Sub-Saharan Africa. Reduced multilateral funding risks slowing progress on energy access, sustainability, and climate goals. As financial commitments waver, multilateralism faces growing strain, endangering long-term investments in the region’s energy transition and resilience.

Access to renewable electricity is a catalyst for economic growth, better healthcare, and education, driving long-term development. Clean electrification fuels business growth, innovation, and essential services, strengthening social and economic resilience. However, access to capital and the cost of that capital remain key barriers to unlocking these transformative opportunities, and the faster they are overcome, the bigger the accrued benefits over time.

Investing in Africa is crucial as the region has the potential to drive the next wave of global economic growth, especially given that it will have a big portion of the world’s working-age population and because the African Continental Free Trade Area (AfCFTA), commenced January 2021, will provide for a more conducive business and trade environment. Expanding access to clean energy is key to boosting Sub-Saharan Africa’s productivity growth from 1% to 4%, a level that could significantly accelerate development. At that pace, the region could potentially contribute 10% of global output and a fifth of global growth by 2050, making it an essential player in the world economy (The Economist, 2025).

References

Calcaterra, M. et al. (2024). ’Reducing the cost of capital to finance the energy transition in developing countries’. Nature Energy. Volume 9. https://www.nature.com/articles/s41560-024-01606-7

DNV (2024). Energy Transition Outlook 2024. https://www.dnv.com/energy-transition-outlook/download/

Duma, D., Cabré, M.M. (2024). Examining the role of risk mitigation and transfer for renewable energy investments: case studies in West and Central Africa. Stockholm Environment Institute. https://doi.org/10.51414/sei2024.060

Hafner, M. et al. (2018). Energy in Africa - Challenges and Opportunities. https://library.oapen.org/bitstream/handle/20.500.12657/23296/1006859.pdf?sequence=1

IEA ─ International Energy Agency (2025). How a high cost of capital is holding back energy development in Kenya and Senegal. February. https://www.iea.org/commentaries/how-a-high-cost-of-capital-is-holding-back-energy-development-in-kenya-and-senegal

IEA (2023). Financing Clean Energy in Africa - World Energy Outlook Special Report. https://www.iea.org/reports/financing-clean-energy-in-africa

IEA (2020). The Covid-19 crisis is reversing progress on energy access in Africa. https://www.iea.org/articles/the-covid-19-crisis-is-reversing-progress-on-energy-access-in-africa

IRENA ─ International Renewable Energy Agency (2024). Sub-Saharan Africa - Policies and finance for renewable energy deployment https://www.irena.org/Publications/2024/Jul/Sub-Saharan-Africa-Policies-and-finance-for-renewable-energy-deployment

IRENA, Climate Policy Initiative (2023). Global landscape of renewable finance 2023. https://www.irena.org/Publications/2023/Feb/Global-landscape-of-renewable-energy-finance-2023

IRENA (2016). Unlocking renewable energy investment: The role of risk mitigation and structured finance. https://www.irena.org/publications/2016/Jun/%20%20%20%20Unlocking-Renewable-Energy-Investment-The-role-of-risk-mitigation-and-structured-finance

IMF – International Monetary Fund (2024). Harnessing Renewables in Sub-Saharan Africa: Barriers, Reforms, and Economic Prospects. https://www.imf.org/en/Publications/staff-climate-notes/Issues/2024/10/08/Harnessing-Renewables-in-Sub-Saharan-Africa-Barriers-Reforms-and-Economic-Prospects-555077

OECD (2024) Developed countries materially surpassed their USD 100 billion climate finance commitment in 2022. https://www.oecd.org/en/about/news/press-releases/2024/05/developed-countries-materially-surpassed-their-usd-100-billion-climate-finance-commitment-in-2022-oecd.html

SEforAll (2022). Nigeria Energy Transition Plan. https://www.seforall.org/our-work/initiatives-projects/energy-transition-plans/nigeria

Singh, H. et al. (2019). ‘The energy transitions index: An analytic framework for understanding the evolving global energy system’. Energy Strategy Reviews. Volume 26, November. https://doi.org/10.1016/j.esr.2019.100382

Tamele, B. et al. (2025). ‘Electricity consumption and its determinants in rural Mozambique – At the edge of the electricity grid’. Energy for Sustainable Development. Volume 85. April. https://www.sciencedirect.com/science/article/pii/S0973082625000122#f0025

The Economist (2025) The Africa Gap – Special Reports

UNCTAD (2024) Countries agree $300 billion by 2035 for new climate finance goal – what next? 10 December. https://unctad.org/news/countries-agree-300-billion-2035-new-climate-finance-goal-what-next

UNCTAD (2023) Commodities at a glance: Special issue on access to energy in Sub-Saharan Africa. https://unctad.org/publication/commodities-glance-special-issue-access-energy-sub-saharan-africa

4/10/2025 9:00:00 AM