Gulf of Mexico: Second offshore wind auction brings waves of opportunity

We are invested in the region developing solutions to harness the innovation opportunities associated with offshore wind deployment.

Introduction

Offshore wind development in the United States (U.S.) Gulf of Mexico (GOM) has its challenges; however, offshore wind leasing in the region is expected to continue. DNV has a strong presence in the GOM and has supported offshore and port operations for decades. Specific to offshore wind, over the last four years, our team has conducted several feasibility and risk assessments, permitting and stakeholder-focused projects, and technological evaluations of the region and specific lease areas. Given our experience, we understand why low wind speeds, soft soil conditions, hurricanes, existing oil and gas (O&G) infrastructure, and uncertain offtake mechanisms have made headlines as obstacles rather than opportunities for innovation. When the first ever offshore wind auction (GOMW-1) was held in the region, all eyes were on the value the three lease areas would receive from the 16 pre-qualified bidders. While only two participants bid for a single lease area over two rounds, it was a testament to the growing interest in this sector. The two areas located off the coast of Texas received no bids, and the area off the coast of Louisiana (OCS-G37334) was awarded to RWE Offshore US Gulf, LLC for USD 5.6 million.

In this light, just because bidders held back during the first auction, it does not mean that the outcome will be the same in the upcoming lease sale. Fast forwarding to March 21 of this year, the Proposed Sale Notice (PSN), outlining terms for the upcoming (GOMW-2) auction, was issued and has initiated the 60-day public comment leading to release of the Final Sale Notice (FSN). For this GOMW-2 auction, the Bureau of Ocean Energy Management (BOEM) has proposed four lease areas off the coast of Texas and Louisiana for a total area of 410,060 acres on the Outer Continental Shelf (OCS) (depiction below).

Auctions: Compare and contrast

Similar to the GOMW-1 lease auction held in August 2023, a multiple-factor auction format is proposed for the upcoming GOMW-2 lease auction. The bid can consist of two parts, a monetary factor (cash bid) and up to two non-monetary factors in the form of bidding credits. DNV has successfully developed applications to BOEM for bidding credits on behalf of customers through development of a conceptual strategy—with region-specific considerations and evaluation of fisheries, supply chain, workforce, port uses, and stakeholder groups. We anticipate similar consideration, and a hyper-local focus, to be imposed in GOMW-2 as BOEM evaluates whether the full, partial, or no amount is to be credited. Table 1 summarizes the changes to the bidding credits which have a different weight compared to the previous auction and changes to the auction rules.

Table 1: Potential differences in Gulf of Mexico lease sale auctions, pending issuance of Final Sale Notice

| Topic | GOMW–2 | GOMW–1 |

| Auction Rule: Bids per Round | Submit bids for multiple lease area per round | Submit on single lease area per round |

| Auction Rule: Number of Lease Areas per Bidder | Unlimited | One Lease |

| Bidding Credit: Domestic Supply Chain and Workforce Development | Up to 17% | Up to 20% |

| Bidding Credit: Fisheries | Up to 8% | Up to 10% |

In addition to the above, BOEM has also changed the rules on the number of lease areas that can be acquired. Whereas in GOMW-1 the bidder was limited to one lease area, the GOMW-2 auction allows to bid on several and theoretically all four areas. Also, unlike several other offshore wind auctions held to date, the states neighboring the GOM lease areas lack specific offshore wind targets mandated by law. Instead, offshore wind energy generated in this region is more likely to be directly sold to large industrial customers or serve as an enabler of green hydrogen production. By allowing lessees to secure multiple lease areas, BOEM anticipates achieving economies of scale and promoting efficient development, which increases the commercial attractiveness of projects.

What are the opportunities?

Existing infrastructure

The O&G industry has played a significant role in the development of the region—and it has become nationally recognized for its energy resources and infrastructure. According to the U.S. Energy Information Administration (EIA), approximately 15% of the total U.S. crude oil is produced offshore in federal waters of the GOM while over 47% of the total U.S. petroleum refining operations take place along the Gulf coast. The support of O&G exploration, development, and transport has already led to significant infrastructure and supply chain being established along the Gulf Coast and includes ageing assets that can be repurposed for renewable energy generation and transport.

What this means: Under the right conditions, the existing infrastructure can be reused for renewable energy projects, increasing the commercial attractiveness of a project in the GOM while reducing the carbon footprint in comparison to a greenfield development. While the GOM may have a comparatively lower wind energy resource than the Atlantic and Pacific coasts, and despite the risks of extreme weather and offtake uncertainty, it is important to remember that these challenges pave the way for extraordinary opportunities and innovation. Unique to this region, existing infrastructure can support not only offshore wind energy generation but potentially green hydrogen production and transport, established port infrastructure and supply chain, and a skilled workforce that benefits national offshore wind ambitions.

A framework for how to repurpose existing O&G infrastructure has not been defined; however, the renewable energy and O&G industries are working collectively to develop a framework as part of the ROICE (Repurposing Offshore Infrastructure for Clean Energy) that addresses asset suitability for repurposing and regulatory and permitting pathway for potentially co-existing with or converting O&G leases to renewable energy leases.

Offtake creativity

The commercial opportunity in the GOM is going to require creativity. Offshore wind energy production here will be competing with onshore wind, which remains more cost-effective. Additionally, and as previously mentioned, state mandated offshore wind energy procurement targets do not exist and the electrical service territories operating in the region do not provide the required market structure to support offshore wind.

The Electricity Reliability Council of Texas (ERCOT) region is a deregulated market without large centrally controlled utilities. There is no capacity market which would hold generators liable to ensure that there is enough power to meet the peak demands. With corporate offtakes being the norm, onshore wind and solar displace offshore wind in terms of cost. Alternatively, the Midcontinent Independent System Operator (MISO) is a wholesale capacity market with a small number of vertically integrated utilities which are responsible for generation, transmission, and distribution with little transmission capacity connection between MISO South and MISO North and Central. Although the MISO structure and policies are supportive of offshore wind, similar to ERCOT, offshore generation struggles to compete with solar, onshore wind, and natural gas.

In 2023, the Department of Energy (DOE) announced that it selected HyVelocity to develop a Gulf Coast Hydrogen Hub which will build on the existing hydrogen production facilities and pipelines to scale the clean hydrogen supply and demand in the GOM. Given the challenges of the electricity market and lack of state policies supporting offshore wind, zero carbon hydrogen can be the most likely offtake alternative considering that it has been incentivized by the Inflation Reduction Act (IRA). Arguably, and based on our project experiences and research within the region, the potential to combine offshore wind energy offtake with green hydrogen offtake can provide a commercial pathway for projects if increasing the scale of projects is considered.

To this effect, DNV continues to support developers in the region to identify offtake options. With deep understanding of the region, DNV’s expertise has been sought out to conduct grid interconnection assessments identifying potential interconnections for offshore wind projects and supported in developing hydrogen permitting frameworks.

Discussion and outlook

It remains to be seen whether the changes made to the PSN, compared to the previous auction conditions, will carry over to the FSN and yield award of all lease areas being auctioned by BOEM in the fall. Similar to the previous auction, the two lease areas situated in closer proximity to the Louisiana border could potentially be more appealing to bidders. Additionally, the inclusion of producing hydrogen or other energy products within the lease may result in a different auction outcome.

Existing infrastructure and skilled workforce supportive of offshore wind and hydrogen production in the GOM can be a lever to increase commercial attractiveness of projects. Even with the challenges described previously it is clear that offshore wind leasing in the region is expected to continue.

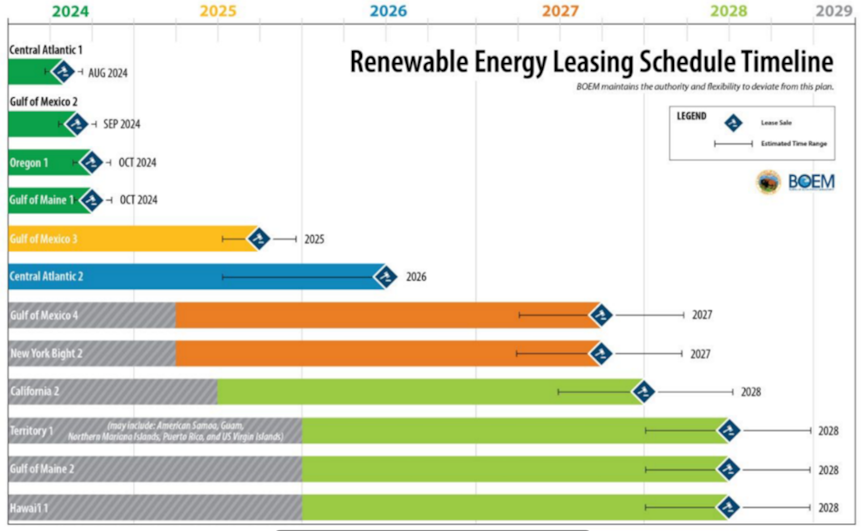

On April 24, 2024, BOEM announced a new five-year offshore wind leasing schedule which includes 12 lease sales across the Atlantic, GOM, Pacific, and offshore U.S. territories. Of the 12 lease sales, three are expected to occur in the GOM with the GOMW-2 auction expected to occur in late Q3 2024. The new five-year offshore wind leasing schedule provides assurance to developers, OEMs, infrastructure partners and relevant state authorities that offshore wind is still in its infancy stages in the U.S. and there is more to come on the horizon.

DNV maintains a robust foothold in the GOM region, anchoring its American headquarters in Houston. Over decades, our local experts have provided support to clients in renewables (onshore and offshore), O&G, and maritime sectors, demonstrating an acute understanding of the region's unique opportunities. We are invested in the region and look forward to innovating and developing solutions in collaboration with our customers to harness the innovation opportunities associated with offshore wind deployment.

Relevant Links

- PSN: https://www.federalregister.gov/documents/2024/03/21/2024-05955/gulf-of-mexico-wind-lease-sale-gomw-2-for-commercial-leasing-for-wind-power-on-the-outer-continental

- Carman, Kristin, DNV Energy USA, Inc. Whitepaper, Offshore wind: prospects within the Gulf of Mexico. July 2023

- https://www.offshorewind.biz/2023/04/28/offshore-wind-in-the-gulf-of-mexico-holistic-project-approach-indicates-promising-opportunity/

- https://www.eia.gov/special/gulf_of_mexico/

- https://www.hyvelocityhub.com/support/hyvelocity-selected-to-develop-gulf-coast-hydrogen-hub/

- https://www.doi.gov/pressreleases/secretary-haaland-announces-new-five-year-offshore-wind-leasing-schedule

5/29/2024 1:00:00 PM